GST updates and its new features – GST Registration in Coimbatore

GST registration in Coimbatore

GST registration can be done with the special offers and with higher efficacy.

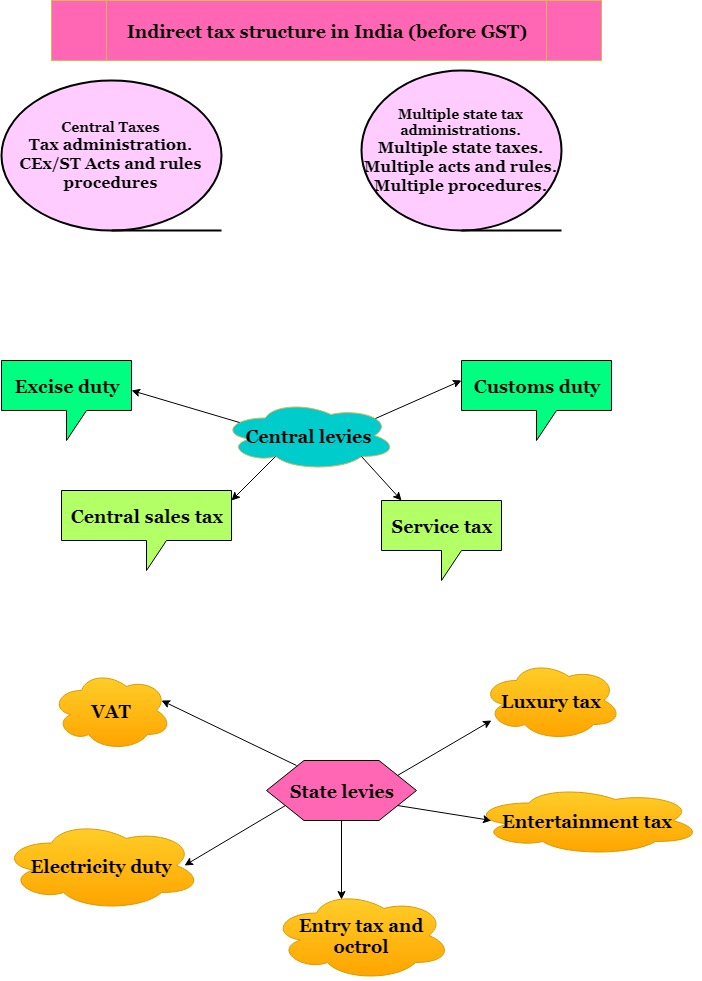

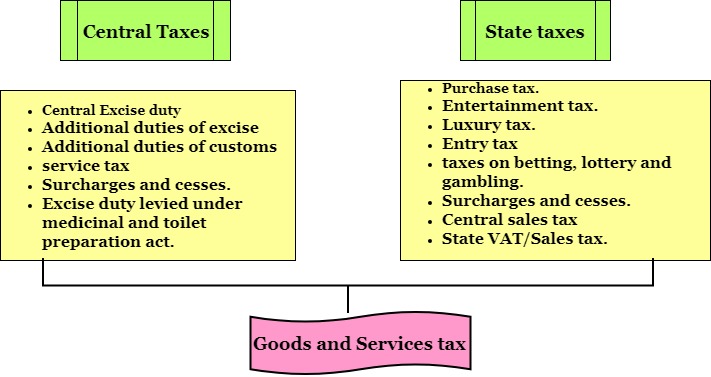

Goods and services tax (GST) means any tax on the supply of goods, services or both except the taxes on the supply of the alcoholic liquor for the human consumption. It has unique principles and significant elements of prior central and state laws. It is actually inspired by VAT/GST legislation of Australia, Malaysia, and EU etc. along with the international VAT/GST guidelines of The Organisation for Economic Cooperation and Development (OECD).

Article 366 (12) – goods (It includes all the materials, commodities and articles.

Article 366(26A) – Anything other than the goods.

Article 366(26b) – With reference to the articles 268, 246A, 269, 269A and 279A includes a union territory with the legislature.

GST council decisions:

- Threshold limit for exemption is Rs.20 lac. (For special category states –Rs.10 lac). Except for J&K.

- Threshold limit for compounding scheme is Rs.1 Crore.

- For traders – 1%.

- For manufacturers -2%

- For restaurants – 5%.

- This turnover limit has been recommended to be raised to Rs.1.5 Crore in 23rd amendment in the act.

- Existing area based exemption schemes can be converted into reimbursement based schemes by government.

- Tax rates are 5%, 12%, 18% and 28%.

- Separate tax rate of 3% or 0.5% for precious metals.

- Some goods and services would be exempt.

- Tax on the peak rate of 28% on specified luxury goods.

- To ensure the single interface –all administrative control over.

- 90% of tax payers whose turnover below Rs.1.5 Crore would vest with the state tax administration.

- Tax payers of 10% whose turnover below Rs.1.5 Crore may vest with the central tax administration.

- Taxpayers having turnover above Rs.1.5 crore would be divided equally between the central and state tax administration.

- With the power of IGST act, it shall be cross empowered on the same basis as under CGST and SGST acts with the few exceptions.

- There are around eighteen rules have been recommended and notified for Composition, valuation, registration and input tax credits, etc.

Exemption from registration:

- To suppliers who provide the services through an e-commerce platform provided that their aggregate turnover shouldn’t exceed the amount of Rs.20 lacs.

- To the suppliers who make the inter-state supply up to Rs.20 lacs.

- Reverse charge on purchase from the unregistered persons –exemption from the section 9(4).

- There is no requirement to pay the tax on advance which has been received for the supply of goods by all the taxpayers.

- Exemption from the tax for the supplies when it is from the goods transport agency (GTA) to the unregistered person.

- TCS/TDS provisions will be suspended till 31/3/18.

- E-wallet scheme for the exports will be introduced from 1/4/18.

Nationwide E-way bill will be introduced for the inter-state supplies from 1/2/18 and for the intra-state supplies from 1/6/18.

- All the taxpayers are required to file GSTR-3B monthly and have to pay the tax on monthly basis.

- Tax payers whose turnover up to Rs.1.5 Crore need to file GSTR-1 returns quarterly and monthly for the other taxpayers.

- The time duration for filing GSTR-2 and GSTR-3 for the months of July 2017 to March 2018 would be worked out by a committee of officers.

- The late fee has been already paid but subsequently waived off will be re-credited to their electronic cash ledger under the tax head instead of Fee head.

- There is a facility of manual filing for refund the application and for advance ruling.

- If the tax liability for the month is “NIL”, it will be charged of Rs.20 per day instead of Rs.200.

- If the tax liability for that month is not “Nil’, it will be charged of Rs.50 per day instead of 200.

- Services for Nepal and Bhutan will be exempted from GST if the payment has not received in foreign convertible currency; those suppliers will be eligible for input tax credit.

- The centralised Unique Identification Number (UIN) will be issued to every foreign diplomatic mission/UN organisation by the central government.

Features of GST act:

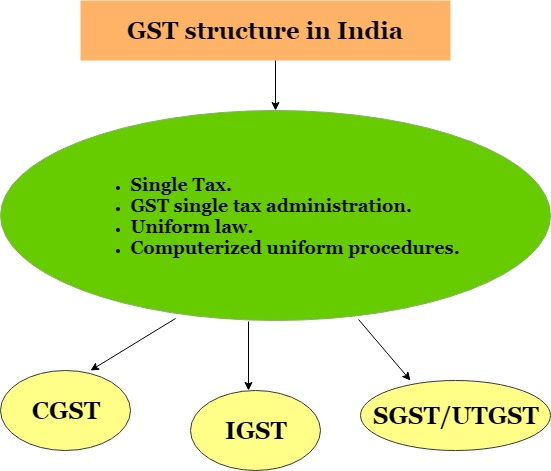

- Concurrent jurisdiction for levy and collection of GST by the centre and the states.

- Centre to levy and collect the IGST on supplies in the course of interstate supplies and imports.

- All transactions and processes only through the electronic mode – non-intrusive administration.

- Compensation for the loss of revenue to states for five years.

- PAN based registration.

- Registration can be done only if the turnover is more than Rs.20 lac.

- Composition scheme will not be available for the inter-state suppliers, specified category of manufacturers and the service providers (Except restaurant service).

- Input tax credits may be available on taxes paid on all the procurement.

- There is an option of voluntary registration.

- Set of auto populated annual and monthly returns.

- Automatic generation of returns.

- Composition tax payers to file the quarterly returns.

- GST practitioners for assisting the filing of returns.

- GSTN and GSPs (GST Suvidha Providers) to provide the technology based assistance.

- Refunds will be granted within 60 days.

- Refunds will be directly credited to the bank accounts.

- Comprehensive transitional provisions for the smooth transition of existing tax payers to the GST regime.

- State level screening committee has to set up.

We are a team of professional experts who provides the brilliant solutions to the clients for all their business related issues and requirements. GST registration can be done within the shortest duration of time and at a reasonable cost. To know more details -> Go here.