GST payments and refunds – GST Registration in Coimbatore

GST payments and refunds:

If a dealer once files a GSTR-1 and GSTR-2, then they are required to file a GSTR-3 and can make the GST payment. If a refund is required to be claimed, the same could be done by filing the relevant refund related forms.

Payments to be made under GST:

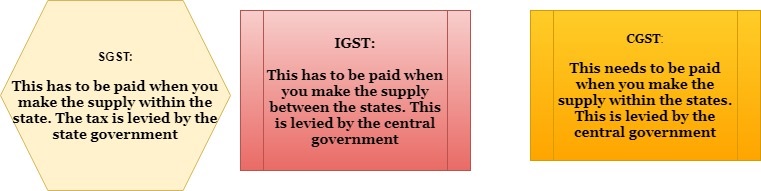

As per GST, the tax which is to be paid is mainly divided into three categories. They are:

For instance,

If you sell any goods from Delhi to Bombay, you need to pay the tax for CGST and SGST not for IGST because; the supply has been done within the states.

If you sell any goods within Bombay, you are required to pay the tax for IGST since the supply has been done within the particular state.

Apart from the above-mentioned taxes, a dealer is required to make these payments. They are as follows:

Tax deducted at source (TDS)-

TDS is a mechanism in which the tax would be deducted by the dealer before making the payment to the supplier.

For example:

The contracting agency gives a road laying contract to a builder; the contract value is Rs.10 lakh.

When the government agency makes a payment to the builder TDS @1% (which amount to Rs.10000) that will be deducted and the balance amount will be paid.

Tax collected at source (TCS):

It is mainly for e-commerce aggregators which mean any dealer selling through e-commerce will receive the payment after deduction of TCS @ 2%.

This provision is currently relaxed and would not be applicable to notified by the government.

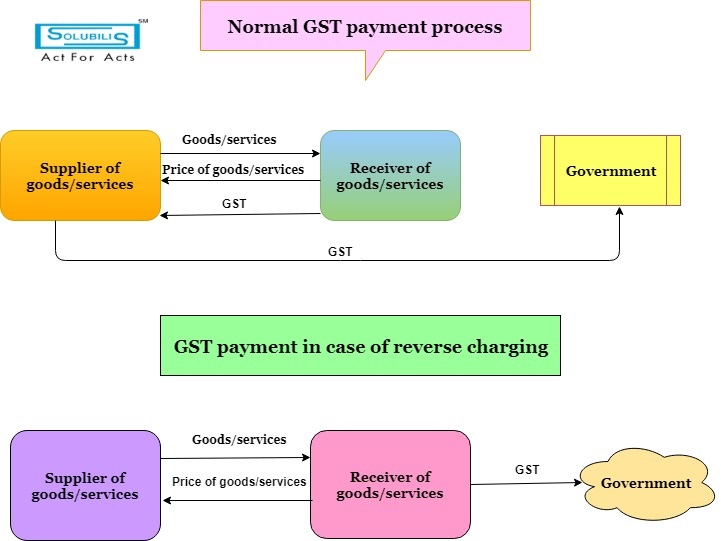

Reverse charge:

When the payment liability shifts from the supplier of goods and services to the receiver are called reverse charging.

GST payment process in a diagram:

Calculate GST payment:

Actually, the input tax credit has to be reduced from outward tax liability in order to calculate the total GST payments to be made.

TCS and the TDS have reduced from the total GST to arrive at the net payable figure. Late fee and the interest will be added to arrive at the final amount.

Input tax credit also cannot be claimed on interest and late fees. This late fee and the interest are required to be paid in cash.

The calculation is different for different types of dealers. They are as follows:

Regular dealer:

A regular dealer is the one who is liable to pay GST on the outward supplies made and also can claim Input Tax Credit (ITC) on the purchase made by him.

GST which is payable by a regular dealer is the difference between the outward tax liability and ITC.

Composition dealer:

GST payment for a composition dealer is comparatively simpler. A dealer who opts for composition scheme needs to pay a fixed percentage of GST on the total outward supplies made.

| Composition Scheme | |||

| Type of business | CGST | SGST | Total |

| Manufacturer and traders (Goods) | 0.5% | 0.5% | 1.0% |

| Restaurants not serving alcohol | 2.5% | 2.5% | 5% |

| Service providers are not eligible for composition scheme | |||

Who should make the payment?

Below mentioned dealers are required to make the GST payment:

- A registered dealer needs to make the GST payment if any GST liability exists.

- A registered dealer is required to pay the tax under the reverse charge mechanism.

- E-commerce operator is required to collect and pay TCS.

- Dealers are required to deduct TDS.

When the payment has to be made?

GST payment has to be made within 20th of every month, then only we can able to file GSTR 3B.

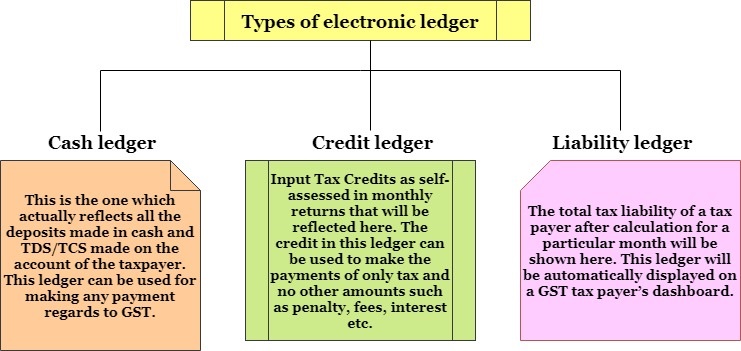

Electronic ledgers:

This is actually maintained electronically on the GST portal.

Ways to make GST payments:

Payment through Credit ledger:

The credits from the “Input Tax Credits” can be taken by dealers for GST payment. The credits can be taken only for the payment of tax. Penalty, interest and the late fees cannot be paid for utilizing the ITC.

Payment through cash ledger:

The GST payment can be made online or offline but the challan has to be generated on GST portal for both the online and offline GST payment.

If the tax liability is more than Rs.10, 000 then it is mandatory to pay taxes online.

The penalty for delayed or non-payment:

If GST is unpaid or short paid or late paid, interest at a rate of 18% is required to be paid by the dealer.

The penalty also needs to be paid. The penalty may be higher than Rs.10, 000 or 10% of the tax unpaid or short paid.

GST refund:

When the GST paid is more than the GST liability, a situation of claiming GST refund may arise. As per GST, the process of claiming a refund has been standardized in order to avoid the confusion. The process is online and the time limits also been set for the same.

When can that refund be claimed?

There are many cases where the refund can be claimed. Some of them are listed here:

Excess payment of tax has been made only due to the omission or by mistake.

- Dealer exports (including deemed export) goods or services under the claim of refund or rebate.

- Input Tax Credit accumulation due to output being tax exempt or nil rated.

- Refund of tax which is paid on purchases made by UN bodies or embassies.

- Tax refund for international tourists.

- Finalisation of provisional assessment.

To calculate GST refund:

Here, we take a simple example of an excess payment made.

Ms.Halena’s GST liability for the month of March is Rs.30000. But due to mistake, she had done the payment of Rs.3 lakh.

Now, she has made an excess GST payment of Rs.2, 70,000 which can be claimed as a refund amount but the time limit for claiming the refund is 2 years from the date of payment.

Time limit for claiming the refund:

The time limit to refund the amount is 2 years from the particular date.

The date may differ in every case.

| GST refund – the reason for claiming | Relevant date |

| Excess payment of GST | Date of payment |

| Export or the deemed export of goods or services | Date of loading/dispatch/passing the frontier |

| ITC accumulates as output is tax exempt or nil rated | the Last date of the financial year in which the credit belongs |

| Provisional assessment finalization | Date where the tax been adjusted |

If the refund has been paid with delay, an interest of 24% per annum is payable by the government.

How to claim GST refund?

The application for a refund needs to be made in Form RFD 01 within 2 years from the relevant date. The form also has to be certified by the chartered accountant.